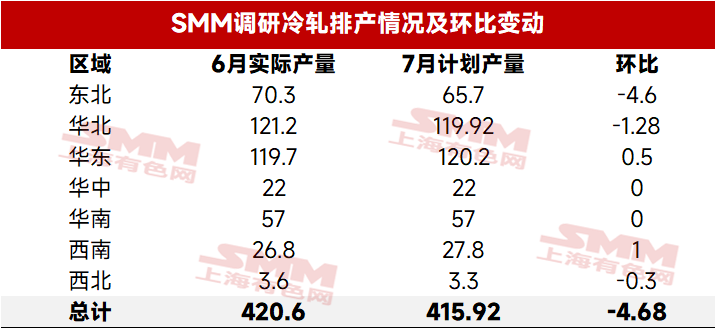

- SMM Cold-rolled Production Schedule: Cold-rolled Production Schedule of Steel Mills Declines Slightly in July

According to the latest SMM survey, the planned production volume of cold-rolled commercial materials for 31 mainstream cold-rolled steel mills in July totaled 4.1592 million mt, a decrease of 46,800 mt compared to the actual production volume of cold-rolled commercial materials in June, representing a 1.11% decline. On a daily average basis, with one more day in July than in June, the planned daily average production volume of cold-rolled materials in July was 134,200 mt, down 4.30% MoM from the actual daily average production volume in June.

Table-1: Month-on-Month Changes in Planned Production Volume of Cold-rolled Commercial Materials at SMM Steel Mills

Source: SMM Steel

Chart-1: Planned Production Volume of Cold-rolled Commercial Materials at SMM Steel Mills

Source: SMM Steel

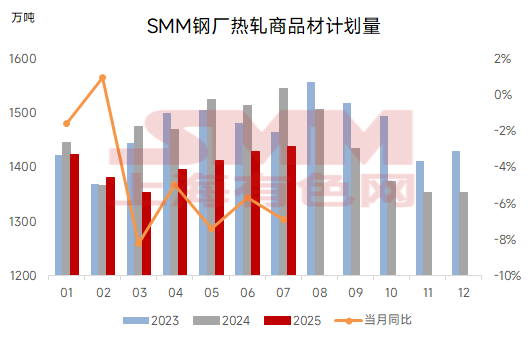

- SMM Hot-rolled Production Schedule: Daily Average Production Schedule of Hot-rolled Materials Declines by 2.7%

According to the latest SMM survey, the planned production volume of hot-rolled commercial materials for 39 mainstream hot-rolled steel mills in July totaled 14.3906 million mt, an increase of 74,900 mt compared to the actual production volume of hot-rolled commercial materials in June, representing a 0.52% increase. On a daily average basis, with one more day in July than in June, the planned daily average production volume of hot-rolled commercial materials in July was 464,200 mt, a decrease of 13,000 mt compared to the actual daily average production volume in June, representing a 2.72% decline.

Chart-2: Planned Production Volume of Hot-rolled Commercial Materials at SMM Steel Mills

Source: SMM Steel

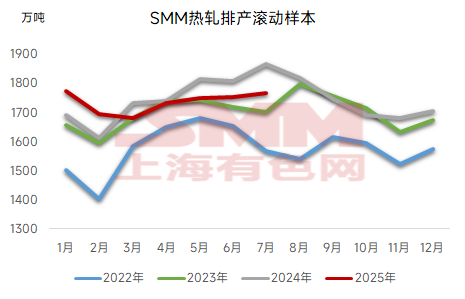

This month, the planned production volume of hot-rolled commercial materials for 52 mainstream hot-rolled steel mills, after the expansion of SMM's sample, totaled 17.6686 million mt, with the daily average planned production volume increasing by 0.13% compared to the actual production volume in June.

Chart-3: Planned Production Volume of Hot-rolled Commercial Materials at SMM Steel Mills (Rolling Sample)

Source: SMM Steel

In July, some steel mills in North and South China concluded maintenance and gradually resumed production. However, as the impact of the off-season gradually emerged, downstream industry orders faced increased pressure, and some steel mills in north China underwent annual maintenance. As a result, the total planned production volume of hot-rolled materials at steel mills in July remained basically stable MoM, while the daily average production schedule declined MoM.

Domestic and Export Trade Analysis:

Domestic Trade: In July, the planned production volume of hot-rolled materials for domestic trade was 13.1806 million mt, with a daily average of 425,200 mt, down 15,400 mt MoM from the actual domestic daily average production volume in June, representing a 3.50% decline.

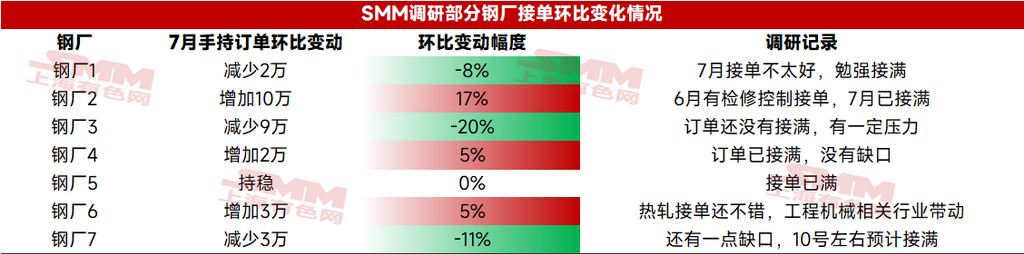

Table-2: Order-Taking Situation at Some Steel Mills Surveyed by SMM

Source: SMM Steel

Source: SMM Steel

According to the SMM survey, as of July 8th, although some sample steel mills still had order gaps, most steel mills' domestic trade orders were basically fully taken. With the increasing impact of the off-season, the order-taking pressure rose MoM compared to June. SMM will continue to track the subsequent order-taking situation.

Export Trade: In July, the planned export volume of hot-rolled materials was 1.21 million mt, an increase of 112,200 mt compared to the actual export volume in June, representing a 10.22% MoM increase. The planned export volume of hot-rolled materials at domestic steel mills in July increased slightly MoM compared to the actual export volume in June.

Chart-4: Planned HRC Export Volume of SMM Steel Mills

Data source: SMM Steel

In terms of maintenance, the impact from HRC maintenance in July is temporarily 384,400 mt, a decrease of 132,600 mt MoM from the previous month. The announced maintenance is mainly concentrated in steel mills in north-east China and the western region. SMM will continue to track the subsequent situation. The specific maintenance details are shown in the following table:

Table 3: HRC Maintenance Data of SMM Steel Mills Data source: SMM Steel

Regarding profitability, based on the SMM survey of steel mills' real-time profitability in HRC production, the current real-time profit of most steel mills is concentrated in the range of profitability > 100 yuan/mt, an increase from the level at the beginning of June. Specifically, about 5% of steel mills reported a current profit loss > 100 yuan/mt; 6% of steel mills reported a current profit loss in the range of 50-100 yuan/mt; 11% of steel mills were at the break-even point; 28% of steel mills reported a current profit in the range of 50-150 yuan/mt, and nearly 50% of steel mills were in the state of profitability > 100 yuan/mt.

Chart-5: Real-time Profitability of HRC in Some SMM Steel Mills Over the Past Two Months

Summary: The planned daily average production of HRC in domestic steel mills in July decreased MoM compared to the actual production in June. This is partly related to the annual maintenance of some northern steel mills and partly due to the increased impact of the off-season, with some steel mills reporting increased difficulty in taking orders, leading to corresponding adjustments in their production schedules.

Looking ahead, in terms of supply, the daily average production schedule of HRC in steel mills in July will decrease slightly MoM, which will alleviate inventory pressure in the spot market to a certain extent. In terms of demand, under the backdrop of the off-season, with frequent high-temperature and rainy weather, the overall demand for steel is under pressure. However, the downstream demand for HRC and steel exports are expected to maintain strong resilience.

In addition, on the macro front, at the beginning of July, the central government once again mentioned promoting the orderly withdrawal of backward production capacity, regulating enterprises' low-price and disorderly competition in accordance with laws and regulations, and rectifying "cut-throat competition," which instantly sparked a wave of enthusiasm and drove up ferrous metals series prices. Against the backdrop of the dual policy "warm winds" of "anti-cut-throat competition" and the Political Bureau meeting, market sentiment has recovered. It is expected that the average price of HRC in July will rise slightly. However, the overall pullback in steel demand during the off-season will limit the upside room for HRC prices.

![The most-traded BC copper contract closed down 2.85%, as speculative fervor cooled, weighing on copper prices [SMM BC Copper Review]](https://imgqn.smm.cn/usercenter/CYktX20251217171711.jpg)

![The Black Industrial Chain Lacked Upward or Downward Momentum Before the Holiday [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/FRcmT20251217171746.jpg)

![The most-traded SHFE tin contract plummeted more than 8% in a single day, and tin prices are expected to remain in the doldrums in the short term [SMM Tin Futures Review]](https://imgqn.smm.cn/usercenter/LLUUJ20251217171751.jpeg)